The New York State Retirement System (NYSRS) is one of the largest and most comprehensive pension systems in the country, providing retirement benefits to public employees across the state. Whether you're a teacher, police officer, firefighter, or municipal worker, the NYS Retirement System offers a structured framework to ensure a secure and comfortable retirement. With multiple tiers and plans tailored to different groups of employees, the system is designed to meet the diverse needs of its members. Understanding how it works is essential for making informed decisions about your future. The NYS Retirement System is more than just a pension plan; it’s a promise made by the state to its employees. Established decades ago, the system has evolved to adapt to changing economic conditions and workforce demographics. It operates under the New York State Comptroller’s Office, which oversees the management of pension funds and ensures compliance with state laws. The system manages billions of dollars in assets, investing in a diversified portfolio to safeguard the financial future of its members. Despite its complexity, the NYS Retirement System is built on principles of fairness, transparency, and sustainability, ensuring that retirees receive the benefits they’ve earned over years of service. For those considering retirement or simply looking to better understand their options, navigating the NYS Retirement System can seem daunting. However, with the right information, you can maximize your benefits and make the most of your contributions. From eligibility requirements to vesting periods, and from retirement options to survivor benefits, this guide will walk you through every aspect of the system. By the end, you’ll have a clear understanding of how the NYS Retirement System works and how it can help you achieve your retirement goals.

Table of Contents

- What is the NYS Retirement System?

- How Does the NYS Retirement System Work?

- Who is Eligible for the NYS Retirement System?

- What Are the Different Tiers in the NYS Retirement System?

- How Can You Maximize Your Benefits in the NYS Retirement System?

- What Are the Common Misconceptions About the NYS Retirement System?

- How Does the NYS Retirement System Compare to Other Pension Plans?

- Frequently Asked Questions About the NYS Retirement System

What is the NYS Retirement System?

The NYS Retirement System, or New York State Retirement System, is a defined benefit pension plan that provides retirement, disability, and death benefits to public employees across New York State. It is administered by the New York State Comptroller’s Office and serves over a million members, including teachers, police officers, firefighters, and other municipal workers. The system operates on a pay-as-you-go model, where current employees’ contributions and investment returns fund the benefits of retirees.

One of the key features of the NYS Retirement System is its tiered structure, which categorizes members based on their date of employment. Each tier has its own set of rules regarding contribution rates, vesting periods, and retirement benefits. This tiered system ensures that the pension plan remains sustainable while adapting to economic and demographic changes. The system also offers survivor benefits, disability pensions, and loan programs, making it a comprehensive solution for public employees’ financial security.

Read also:Can I Eat Granola On Daniel Fast A Comprehensive Guide

Understanding the NYS Retirement System is crucial for anyone planning their retirement. It provides a stable income stream during retirement, protecting members from market volatility and ensuring they can maintain their standard of living. With proper planning and knowledge, members can take full advantage of the benefits offered by the NYS Retirement System.

How Does the NYS Retirement System Work?

The NYS Retirement System operates on a defined benefit plan, meaning that retirees receive a fixed monthly payment based on their years of service and final average salary. Contributions to the system are made by both employees and employers, with the state investing these funds to generate returns. These investments, along with ongoing contributions, ensure that the system remains solvent and can meet its obligations to retirees.

Members of the NYS Retirement System are divided into tiers based on their employment start date. Each tier has specific rules governing contribution rates, vesting periods, and retirement benefits. For example, Tier 6 members, who began their employment after April 1, 2012, contribute a higher percentage of their salary compared to earlier tiers. However, they also benefit from a more sustainable pension model that aligns with modern economic conditions.

Retirement benefits are calculated using a formula that considers factors such as years of service, final average salary, and age at retirement. Members can choose from various retirement options, including full retirement, partial retirement, or deferred retirement, depending on their individual circumstances. The system also offers survivor benefits, ensuring that spouses and dependents are financially protected in the event of a member’s death.

Who is Eligible for the NYS Retirement System?

Eligibility for the NYS Retirement System is determined by employment status and job classification. Public employees who work for New York State or local governments, including teachers, police officers, firefighters, and municipal workers, are generally eligible to join the system. Membership is automatic for most employees, and contributions begin as soon as they start their jobs.

To qualify for retirement benefits, members must meet specific vesting requirements. Vesting refers to the period of service required to become eligible for a pension. For example, Tier 6 members must complete ten years of service to be vested, while earlier tiers have shorter vesting periods. Once vested, members are entitled to retirement benefits, even if they leave public service before reaching retirement age.

Read also:Best Hospital In Delhi A Comprehensive Guide To Healthcare Excellence

It’s important to note that eligibility criteria may vary depending on the tier and specific plan. For instance, certain plans offer enhanced benefits for hazardous duty positions, such as firefighters and police officers. Understanding your eligibility and the benefits available to you is crucial for making informed decisions about your retirement.

What Are the Different Tiers in the NYS Retirement System?

The NYS Retirement System is divided into six tiers, each with its own set of rules and benefits. These tiers were created to address changes in economic conditions, workforce demographics, and pension funding requirements. Understanding the differences between tiers is essential for maximizing your retirement benefits.

Tier 1 and Tier 2

Tier 1 and Tier 2 members are among the earliest participants in the NYS Retirement System. Tier 1 members, who joined before July 1, 1973, enjoy some of the most generous benefits, including lower contribution rates and shorter vesting periods. Tier 2 members, who began their employment between July 1, 1973, and June 30, 1976, also benefit from favorable terms, though their contribution rates are slightly higher than Tier 1.

- Tier 1: Vesting period of 10 years, lower contribution rates, and higher benefit multipliers.

- Tier 2: Vesting period of 10 years, slightly higher contribution rates than Tier 1, but still favorable terms.

Tier 3 and Tier 4

Tier 3 and Tier 4 members joined the system between 1976 and 2010. These tiers introduced more balanced contribution rates and vesting periods to ensure the system’s sustainability. Tier 3 members, who began their employment between July 1, 1976, and June 30, 1983, have a vesting period of 15 years, while Tier 4 members, who started between July 1, 1983, and December 31, 2009, have a vesting period of 10 years.

- Tier 3: Vesting period of 15 years, moderate contribution rates, and a focus on sustainability.

- Tier 4: Vesting period of 10 years, balanced contribution rates, and widely applicable rules.

Tier 5 and Tier 6

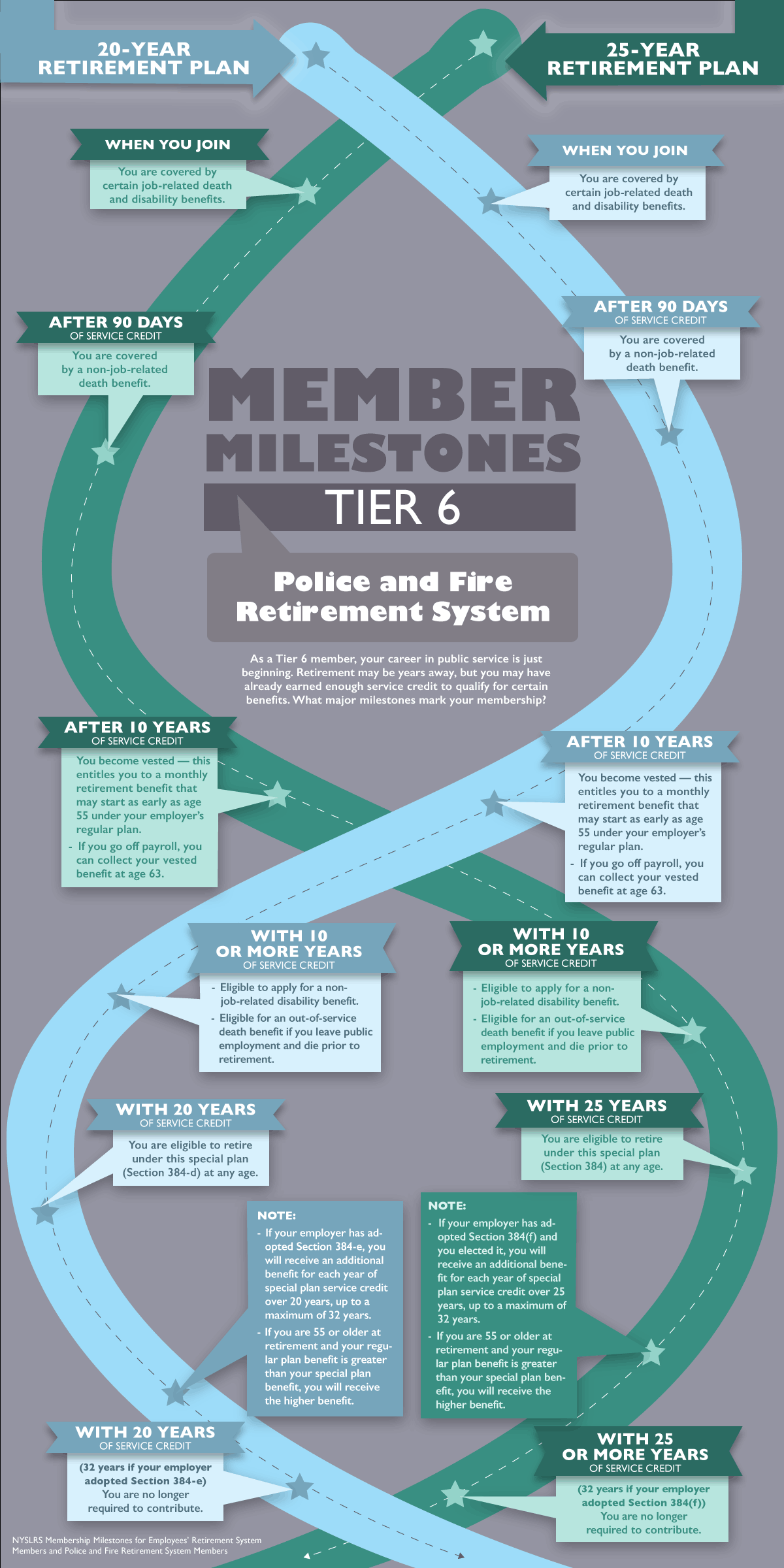

Tier 5 and Tier 6 members are the most recent participants in the NYS Retirement System. Tier 5 members, who began their employment between January 1, 2010, and March 31, 2012, have a vesting period of 10 years and higher contribution rates than earlier tiers. Tier 6 members, who started after April 1, 2012, have the highest contribution rates and a vesting period of 10 years, reflecting the need for a more sustainable pension model.

- Tier 5: Vesting period of 10 years, higher contribution rates, and modernized benefits.

- Tier 6: Vesting period of 10 years, highest contribution rates, and a focus on long-term sustainability.

How Can You Maximize Your Benefits in the NYS Retirement System?

Maximizing your benefits in the NYS Retirement System requires careful planning and a clear understanding of the rules and options available to you. By making informed decisions about contributions, retirement age, and benefit options, you can ensure a secure and comfortable retirement.

Understanding Contribution Rates

Contribution rates vary depending on your tier and employment classification. For example, Tier 6 members contribute a higher percentage of their salary compared to earlier tiers. Understanding how these contributions impact your retirement benefits is crucial for making informed decisions. Members can also choose to make additional voluntary contributions to increase their pension benefits.

Planning for Retirement

Planning for retirement involves considering factors such as your desired retirement age, financial needs, and available benefits. The NYS Retirement System offers tools and resources to help members estimate their retirement benefits and plan accordingly. Members can also consult with financial advisors to create a comprehensive retirement strategy that aligns with their goals.

What Are the Common Misconceptions About the NYS Retirement System?

Despite its widespread use, the NYS Retirement System is often misunderstood. One common misconception is that it is underfunded and at risk of collapse. In reality, the system is well-managed and has consistently met its obligations to retirees. Another misconception is that members can withdraw their contributions if they leave public service. While members can receive a refund of their contributions, they forfeit their pension benefits in the process.

How Does the NYS Retirement System Compare to Other Pension Plans?

The NYS Retirement System stands out for its defined benefit structure, which provides a stable income stream during retirement. In contrast, many private-sector plans have shifted to defined contribution models, such as 401(k) plans, which place the investment risk on employees. The NYS Retirement System’s tiered structure and focus on sustainability also differentiate it from other pension plans, ensuring that it remains viable for future generations.

Frequently Asked Questions About the NYS Retirement System

What happens if I leave public service before retirement?

If you leave public service before retirement, you can either leave your contributions in the system and defer your pension benefits until you reach retirement age or request a refund of your contributions. However, taking a refund means forfeiting your pension benefits.